We need to swap expensive fuel for cheaper finance. And we're asking the banks to step up

More New Zealanders could be running electric vehicles on New Zealand-made energy and saving money from day one. But the bank products that would make EVs more accessible aren't reaching the people who need them most. In Australia, there are much better options available, so why the big gap in interest rates and terms? Why are New Zealanders missing out? We've written to every major bank and the Reserve Bank to fix this.

The problem isn't the cars. It's the finance.

Petrol well over $3/L. Diesel getting up to $4/L. New Zealanders are spending $65 million every day at the pump due to these inflated prices. It used to be $40 million.

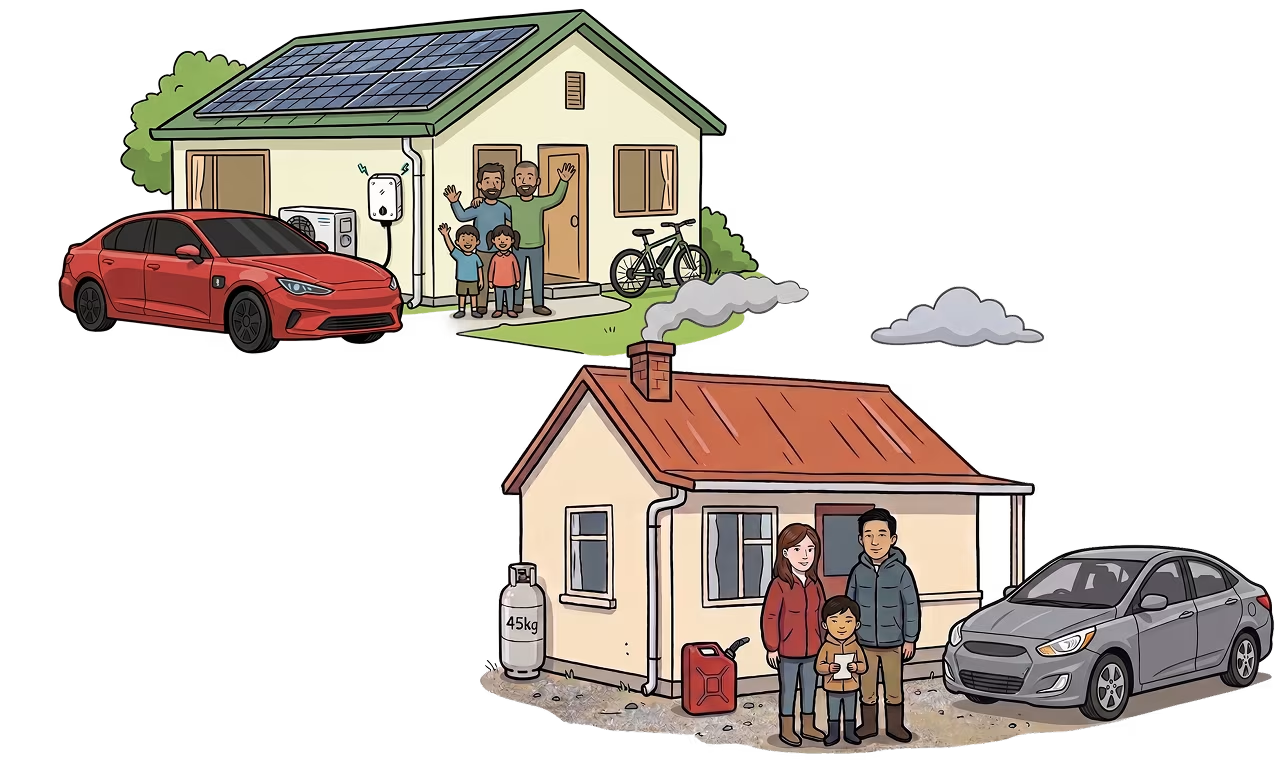

We have the technology to fix this. Electric vehicles running on New Zealand-made energy are cheaper to run from day one. But the barrier is stubbornly financial: the upfront cost keeps EVs out of reach of many households and the bank products that would help close that gap haven't been built.

New Zealand has one of the oldest car fleets in the developed world - average age 14.9 years, with 63% of cars more than ten years old. That's four years older than Australia. Without intervention, many New Zealanders will stay trapped in expensive, ageing fossil-fuel vehicles and will remain vulnerable to wild price swings.

The EV lending gap by the numbers

Our big banks have Australian parents, but New Zealand customers are not getting access to the same products.

Bank EV-finance scoreboard

Every major NZ bank's current offer for someone trying to finance an EV. Updated as offerings change. We'll praise meaningful progress publicly and loudly.

Updated 29 April 2026

| Bank | If you have a mortgage Best deal for homeowners |

If you don't Best deal for renters / no equity |

Verdict |

|---|---|---|---|

| Westpac | 0% 5 yrs · up to $50k · Greater Choices top-up | 7.99% 5 yrs · standalone EV Loan (no mortgage needed) | Best deal |

| ANZ | 1% 3 yrs · up to $80k · Good Energy Home Loan top-up | 13.90% Standard personal loan | Homeowners only |

| ASB | 1% 3 yrs · up to $80k · Better Homes Top-Up | 13.95–19.95% Standard personal loan | Homeowners only |

| BNZ | 1% 3 yrs · up to $80k · Better Future Loan top-up | 13.90% Standard personal loan | Homeowners only |

| The Co-operative Bank | 9.95% Standard personal loan (no green tier) | 9.95% Standard personal loan — lowest standard floor in NZ | No green lending |

| Kiwibank | — EVs explicitly excluded from Sustainable Energy Loan | 13.50% Standard personal loan | EVs excluded |

| SBS Bank | ~13.85% Personal loan via Finance Now subsidiary | ~13.85% Personal loan via Finance Now subsidiary | No green lending |

| TSB | — Discontinued personal lending in 2020 | — Existing customers only — no new applications | No car loans |

Rates and terms reflect each bank's publicly-listed offers as of the date above. "If you have a mortgage" assumes 20%+ home equity with that bank. "If you don't" covers renters, mortgage-free households, and anyone without sufficient equity for a green top-up. Sole traders and businesses may be able to get better rates and terms, so ask your bank.

The solution: low-cost EV finance.

The key to unlocking EVs for Kiwis is finance that matches the asset.

Australia treats car lending as secured — purpose-built EV loans, longer terms (up to seven years), lower rates (from 5.09%). New Zealand banks treat the same loan as an unsecured personal loan — capped at five years, at 7.99%. The kind of product you'd use to buy a second-hand couch.

When you compare a hybrid Toyota RAV4 with a Hyundai Kona EV financed at 5.5% over 15 years, the EV starts saving money from week one — and saves $35,000+ over the lifetime of the vehicle.

Six things we're asking banks to do.

-

1. Extend loan terms on EV loans

Develop a secured EV vehicle loan product — like Australia has — as a distinct offering from the current unsecured personal loan. NZ's EV personal loan market caps terms at five years. Australian lenders offer secured EV loans for up to seven years at lower rates. A move to seven-year terms in NZ would reduce monthly repayments and bring EVs within reach of many more households.

-

2. Reduce interest rates on EV loans

The current market-leader rate for dedicated EV personal loans in NZ sits at 7.99% p.a. Australian lenders are offering equivalent products from 5.09% (secured) and 5.76% (unsecured). We understand the structural differences between the two markets, but there is room to close this gap.

-

3. Broaden eligibility criteria

Loan caps, equity thresholds, and eligible vehicle criteria should be reviewed and updated to reflect the current market — including the growing supply of quality used EVs that represent the most realistic pathway for lower-income New Zealanders.

-

4. Actively and transparently promote your EV loans and other green products

Too many New Zealanders are unaware that preferential green lending even exists. Invest meaningfully in promoting your green and EV loan products with full transparency about the terms — including what happens when any promotional rate period ends.

Customers can be caught off guard when low introductory rates revert to standard rates. Households using a green home loan top-up to purchase an EV today can face a cliff when the promotional term ends. The steps we're asking for would close that gap, allowing households to refinance into a purpose-built product that keeps repayments manageable.

-

5. Create a compelling interim product offering

Don't wait until new products are fully developed before acting. In the interim, introduce an attractive stop-gap offer — a temporarily reduced rate on your existing EV loan, an extended term, or a targeted campaign making your current green products as accessible as possible — so that New Zealanders who need help getting into an EV today are not left waiting while the right long-term solution is built.

-

6. Recognise and communicate the macroeconomic benefits for EV finance

When New Zealanders switch from petrol or diesel to electricity, they stop paying for an imported commodity priced in US dollars and subject to global supply shocks, and start paying for New Zealand-made energy at prices we largely control.

New Zealand currently exports billions of dollars annually to offshore fossil fuel producers — money that leaves our economy permanently. Redirecting even a fraction of that into New Zealand keeps capital circulating, drives productivity, supports business growth, and ultimately expands the very lending market that banks depend on for their own profitability.

Compact SUV, three ways.

At 5.5% interest over 15 years, including upfront cost. Petrol assumed at $3.30/L for 2026 fuel shock.

Who the current products miss.

The banks do offer green home loan top-ups. ANZ, BNZ and ASB lend up to $80,000 at 1% p.a. fixed for three years for EVs, solar, heat pumps and insulation. Westpac's Greater Choices product is 0% for five years on up to $50,000.

But all four require a mortgage with that bank, plus 20% home equity. Renters can't access them. Younger buyers without significant equity can't access them. Mortgage-free households can't access them.

And there's a cliff: the 1% promotional rate expires after three years and reverts to the standard mortgage rate. Households can find themselves with nowhere to refinance into a purpose-built EV product, because that product doesn't exist yet.

Want to know more about EVs?

Range, charging, costs, used vs new, the lot. This Car Can is our deep-dive on what owning an EV in Aotearoa actually looks like.

Visit This Car CanTell your bank you want this

Pick your bank, tick the asks you care about, hit copy. Save the image, paste the post on LinkedIn, tag your bank. Five seconds, real pressure.

Paste the post, attach the image, tag your bank. Done.